kotangens/iStock via Getty Images

kotangens/iStock via Getty Images

It has been a tough few months across the board for most assets as issues due to valuations, inflation, geopolitics, and more wreak havoc on investor sentiment. During such times where no bottom is in sight, it is important to take a step back and reflect on a wide range of companies. This allows you to consider initiating a position in those stocks you have been leaving on your waitlist or find a potential new holding at an opportune entry point. As for this new series of mine, I will be looking at the greenest, most sustainable investments across the market, with a focus on real applications rather than speculative bets. I am sure after this series there will be at least a few “ESG” companies for even the most climate-change-policy-averse investor out there. This article will begin with one of Earth’s reemerging major renewable commodities, forests.

While the tree huggers would disagree, wood products and other forest products are an important economic resource. However, waste is common, and it is important to apply principles of circular and sustainable forestry. With this, we will have plenty of trees in the future to harvest, and process these products with limited carbon resources. While knowledge of the techniques is not important to consider as an investor, it WILL be important to understand different ways to evaluate how sustainable a forest operation is. Sustainable forest management is the process with which we are able to preserve forest environments and obtain valuable resources at the same time.

Forests regulate climate, sequester and store carbon, harbor a large proportion of terrestrial biodiversity, and contribute directly to livelihoods of millions of people who live in or close to forests1-3. The role of forests in achieving sustainability targets has been re-emphasized by national and international sustainability agendas, including the Sustainable Development Goals, the Bonn Challenge, and the Paris Climate Agreement (Hajjar, et al., 2020).

Since forestry is a niche industry in regards to public companies, I will also be covering those paper product producers and distributors who purchase large quantities of timber or forest products from private or government entities. Studies show that while less economically viable in the early years, there is actually much value in thriving and healthy forests in developing regions around the world. However, how do public companies searching for the most shareholder returns fare? After taking a look at the performance of some sustainable forestry companies, I would have to say it is not just small communities that are able to benefit from these developments and that investments in public companies can significantly diversify your portfolio into forestry.

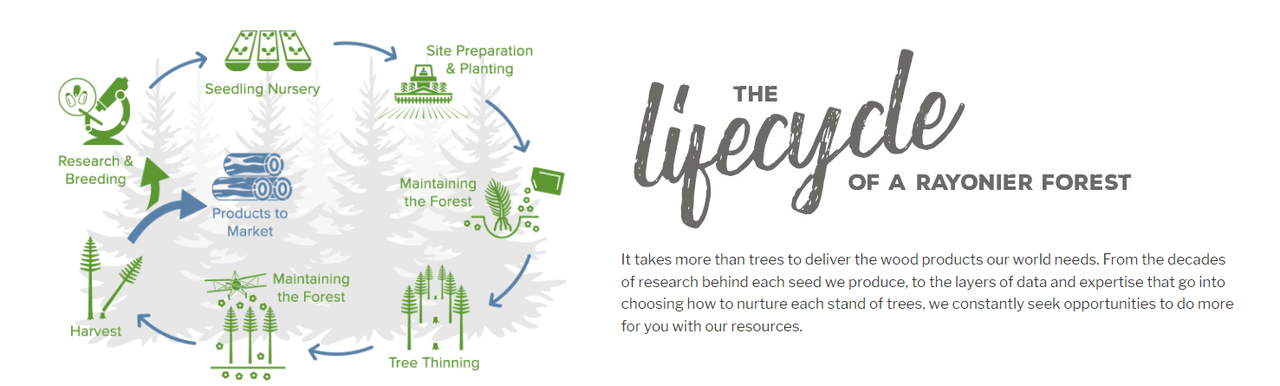

How Sustainable Forest Management Works. (Rayonier)

How Sustainable Forest Management Works. (Rayonier)

Considering the environmental benefits of carbon sequestration, biodiversity, erosion and water cycle control, and even renewable energy generation, there are many positives to a sustainable and circular forest ecosystem. However, it will be important to consider that these investments will be subject to the economic rules of commodities, rather than any alternative. As such, it will be important to consider the asset you invest in, and so I will be discussing some major players later on in the article. I will also be sharing my thoughts and research on the risks and future potential of the industry to shed light on the potential. Let’s begin.

I will start by covering the risks, as those investors who do not wish to have a quite volatile commodity as a holding will want to consider these points first and foremost. The four pillars of risk rotate around Economics, Incentives, Verification, and Competition. As a spectrum of risk, each pillar is influenced by the others, and every public company must be considerate of these factors. There is a reason why this industry still has significant private players and only a few public companies.

The first major consideration revolves around the fact that sustainable forest managers will not be able to produce as much forest product per acre as a one who clear cuts the entire acreage. This issue is rampant in areas where there are no regulations, or these regulations are difficult to maintain (IE. Amazon, Africa, SE Asia). As such, these typically private loggers are able to flood the market with cheap forest products and this is also a competitive factor. However, one of the benefits to sustainable and circular forestry is the fact that there is no end to the available resources, as clear-cutting will have a long wait period between harvests (if they replant trees at all).

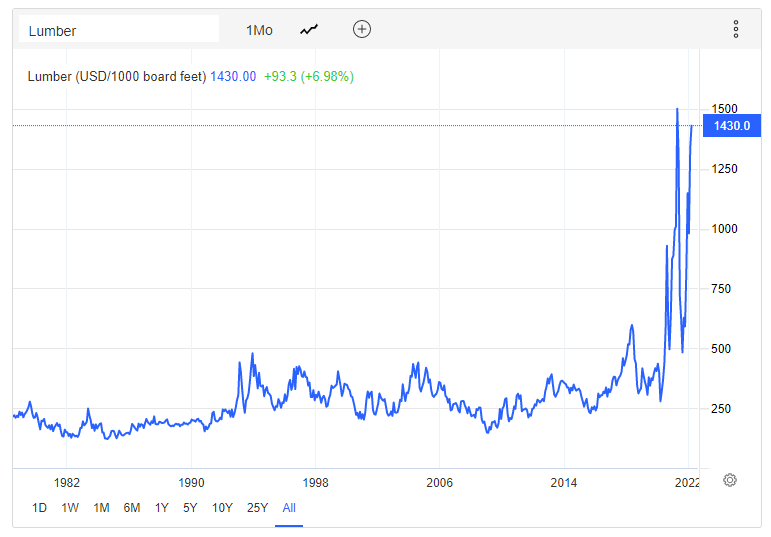

Other economic factors to consider are supply and demand. Lumber prices are quite volatile, especially over the past two years, and this will have a significant impact on share prices for public companies. However, I look quite favorably on the long-term upward trend for the market as there has been a renaissance within the industry of late as the search for renewable technologies has been at the forefront of innovation. I will discuss the future of wood products later on in the article, all of which point to higher demand into the future.

Trading Economics

Trading Economics

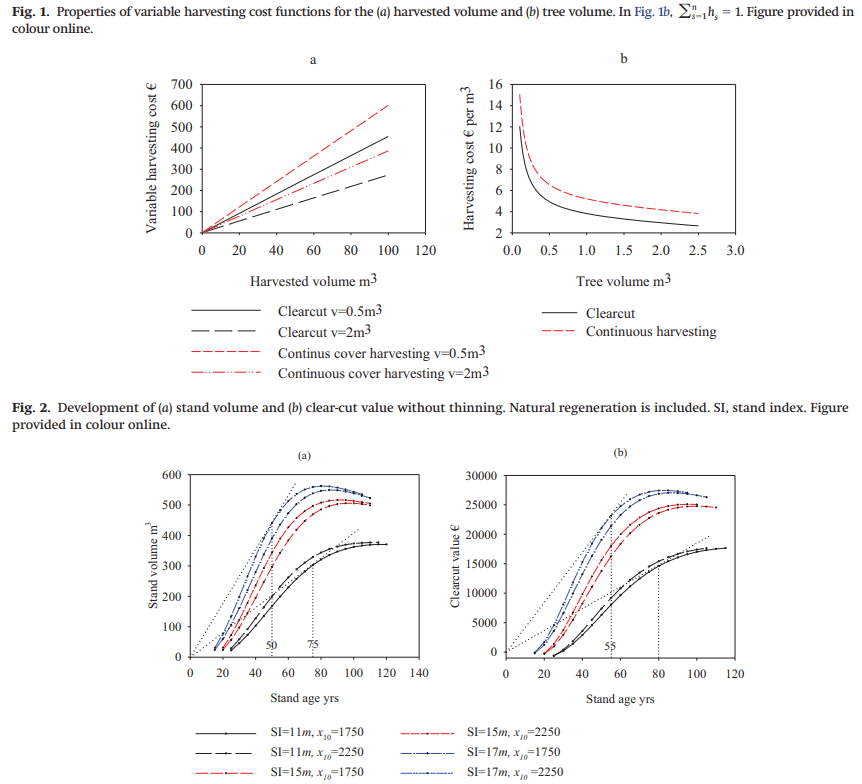

Lastly, as you begin to consider individual landowners or forest operators on a detailed level, it will be important to consider what sustainability technique they use. While I said earlier that knowledge of the techniques is not important, I will make one exception. This is in regards to data on the type of cutting method. The first is clear-cutting over large areas, then allowing for full regeneration before a second harvest. The second is allowing for a full cover to remain at all times and only cutting down a selective number of trees over a larger area. While full cover techniques may be smiled upon more by verification authorities and for the environmental benefits, there is also a tradeoff in the profitability. The chart below, and corresponding research paper, offer a detailed look into these two techniques.

Tahvonen and Rämo 2016

Tahvonen and Rämo 2016

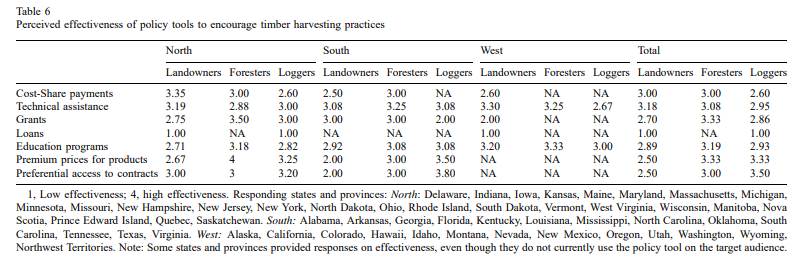

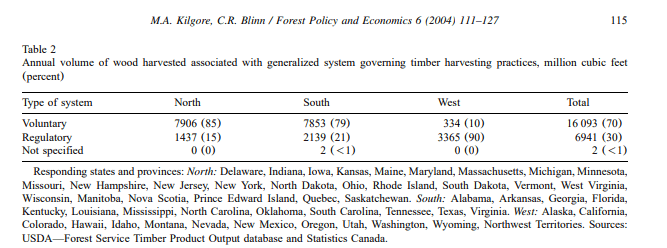

As with many commodities, there are many incentive and other financial programs available. The availability of these incentives vary by region, state, or country, and change based on economic factors. However, they typically increase during times of rising prices and demand, especially during shortages (USFS Paper from 1980). Further, these incentives are necessary for the development of sustainable forest management due to the economic factors I introduced above. The table below sheds light on incentive programs in the US and their effectiveness in encouraging positive harvesting practices in the US and Canada.

…[A]lthough sustainable timber management sometimes provides reasonable rates of return, conventional harvesting is generally more profitable. This implies that without additional incentives, one cannot expect companies to adopt sustainable management (Pearce et al., 2001).

Kilgore and Blinn 2004

Kilgore and Blinn 2004

While incentives are a risk for government regulators and potentially the forest owners, I find that this is now not an issue. As I will discuss later in this article, many customers are now selecting products that are following the necessary regulations. With more capital flowing into sustainable forestry, the current incentives will also allow for a strong financial profile for adherents. Thankfully, all three Timber REITs have favorable accreditation, and may be receiving incentives beyond their REIT status. However, if small businesses are able to obtain better incentives, they may offer competitive risks. It is all quite fluid and typically is untraceable for these public companies so I would not worry until major laws are created.

Due to the rise in ESG investments and considerations, contracts and purchases of lumber are often focused towards sourcing sustainable paper products. However, the issue of verifications is quite complicated. Most of the time, adherence is voluntary, and so a system for third-party verification had to be established. Also, the past decade has seen a rise in adherence around the world in regards to protecting forests and requiring sustainable harvesting, as can be seen with recently enacted Chinese law.

In many cases, sustainable timber management performs better in terms of carbon storage and bio-diversity conservation than conventional logging approaches, as well as producing more timber. If new carbon markets emerge, sustainable forest management might compete effectively with conventional harvesting. Timber certification systems may also provide a sufficient incentive for sustainable forest management in certain conditions (Pearce et al., 2001)

Kilgore and Blinn 2004

Kilgore and Blinn 2004

There are a few major regulatory bodies, but the quality and accuracy of each is variable. The major players are the Forest Stewardship Council (FSC), the Programme for the Endorsement of Forest Certification (PEFC), and the Sustainable Forest Initiative (SFI), although FSC and PEFC offer the highest standards. Each has their own standards and requirements, and transparency regarding the actual state of each forest is often unclear.

When combined with natural factors, such as climate change, the threats to global forest health and integrity are significant (Easterling and Apps 2005). Forest certification for sustainable forest management ([SFM] i.e., forest management that prevents the negative effects of forestry in the long-term while maintaining the benefit to society) emerged in the early 1990s as a remedy to anthropogenic forest degradation (Auld et al. 2008, Vogel 2008)… Despite their existence for more than a decade, little is known about how well forest certification systems achieve their SFM goals. FSC, CSA-SFM, and SFI have been compared on the basis of the wording of their criteria and indicators or on user surveys. As such, we found a strong consensus that FSC certified forests achieve higher levels of sustainable forest management compared to CSA-SFM or SFI (Clark and Kozzar 2011).

However, all three major Timber REITs I will be discussion adhere to most major certification systems, and I believe they do their fair share to create a sustainable and circular forest economy. They will be able to provide shareholders with ample returns for years if they are able to continue using the same plots of land. However, there will always be a risk of inside or outside reporting on these companies that may shed light on failures to develop in a sustainable manner.

The question of who actually controls forest management is quite difficult to understand. As I discussed earlier, most regulations are voluntary in origin, and it will be up to the paper product and distribution companies to discern which loggers are following the specified protocol. However, since most major companies that purchase forest products have announced adherence to many regulatory standards such as FSC and PEFC, larger landowners who have easy access to accreditation may have a slight upper hand. Further, owners of larger tracts of land will be able to leverage higher margin sustainable practices and have a better outcome than small landowners. Although, I cannot find data suggesting possible impacts of economies of scale in timber production.

Many countries have adopted the criteria and indicators (C&I) approach to sustainable forest management, whereby objectives (criteria, e.g., biological diversity, ecosystem condition, and productivity; CCFM 2003) are defined while variables and descriptors (indicators, e.g., area of forest by type, area of forest disturbed by fire; CCFM 2003) are used to evaluate whether objectives are achieved (Goodbody et al., 2020).

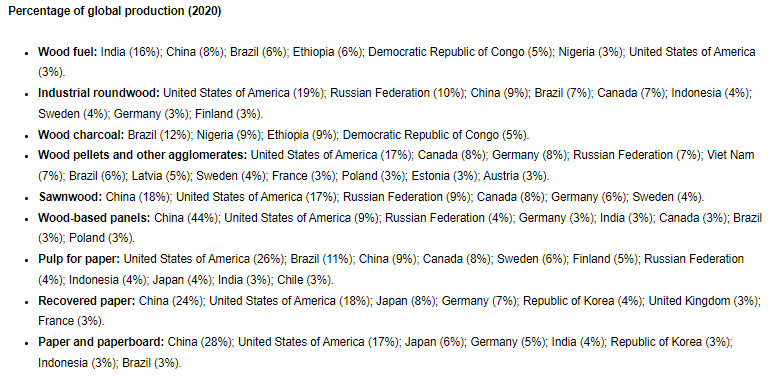

When you want to understand competitive pricing influences, it will be important to know that the top five countries for forest cover, in order, are Russia, Brazil, Canada, the US, and China. As such, macroeconomic factors in these major economies will continue to affect timber prices and competition. With the rise of verification requirements across the world, those who are willing to invest, adhere, and purchase such sustainable wood will see the highest sales growth. As such, there is an ever-shifting production environment worldwide, depending on the type of wood product, as shown in the image below. It will be important to follow news on how these countries verify sustainability, and how they change their production into the future.

Food and Agriculture Organization of United Nations

Food and Agriculture Organization of United Nations

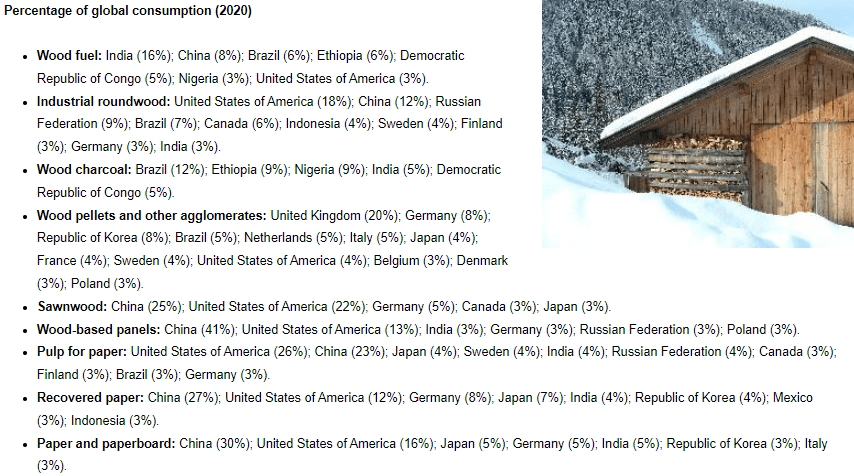

Along with understanding the competition and risks between producers, I will also provide the information I found regarding consumers. This will allow you to consider how the end markets are faring if performing outlook analyses. As you can see, the major economies of the US and China have a significant effect on consumption. As such, watch how those countries are performing across the economy, just as you would for any other commodity. Individual company factors may not have as large of an effect as do economic factors and lumber prices, and this is proven by the strong correlation between all three companies I will be covering.

Food and Agriculture Organization of United Nations

Portfolio Visualizer

Food and Agriculture Organization of United Nations

Portfolio Visualizer

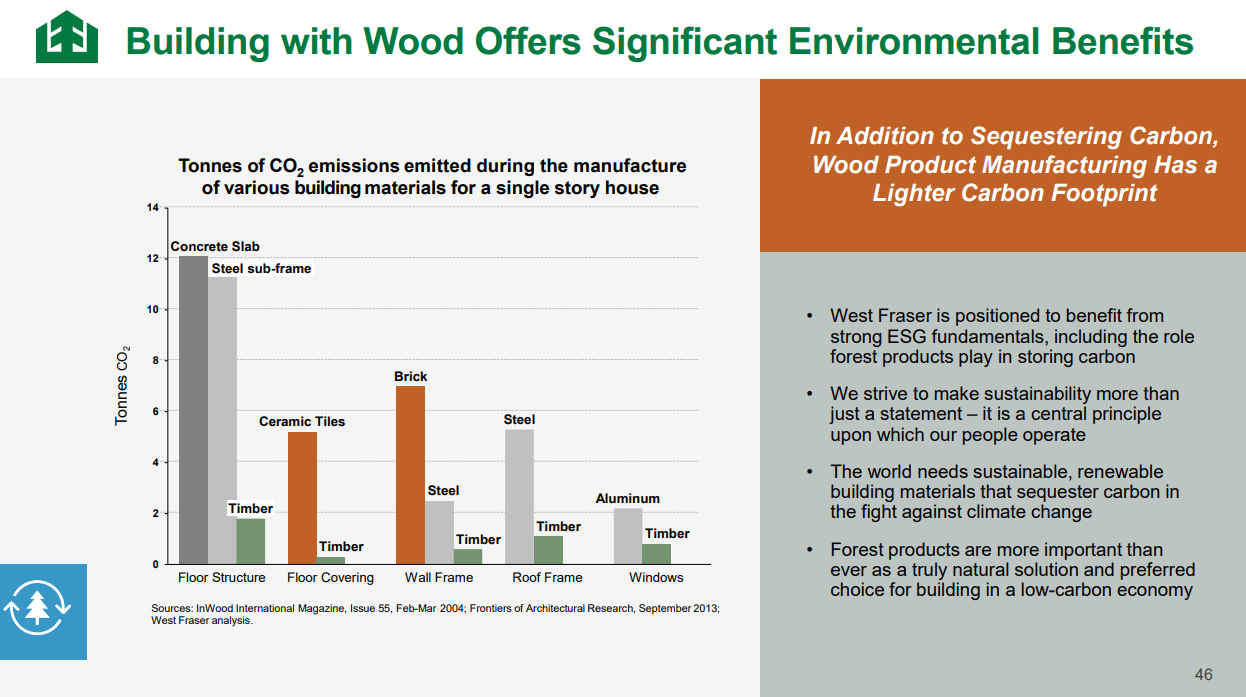

There are dual catalysts that shine favorably on the sustainable forestry industry: new net-zero innovation and adherence. The most favorable aspect of the net-zero movement has been a reevaluation of the forestry industry. As such, there is a renewed focus on sustainable and circular practices, the development of a broader range of end products, and even green energy generation. Interestingly enough, there is even a movement to produce more wood architecture instead of concrete and steel due to their intense carbon requirements. In fact, laminated timber is often regarded as a better building material for some applications and is seeing a resurgence. When architects are considering the ecological impact, wood may begin to provide further competition against concrete and steel in even high-rise infrastructure. However, all of this will require sustainable harvesting and this is why I will be covering the forest owners and operators first.

Wood Innovation Design Center (Ema Peter via Arch Daily)

Wood Innovation Design Center (Ema Peter via Arch Daily)

Beyond demand for novel timber products, there is now also favoritism by investors for sustainability. This will combine the favorable aspects of Verification and Economic risks by driving money into those companies who are able to prove their sustainability. As such, the lower prices of unsustainable forestry will be unable to out-compete this movement of capital into sustainability.

West Fraser

West Fraser

When combined with the environmental benefits, you can see why even countries like Gabon are leveraging sustainable forestry. While this is not an easy factor to track or evaluate, I do believe this favorable sentiment will continue in the future as many companies are accepting these standards. At a certain point, all forestry will be sustainable (although this may not end up favorable for companies at the moment, we will worry about that in the future). Positive verification effects will also become clearer as I discuss mill, paper product, and distribution companies in a future article.

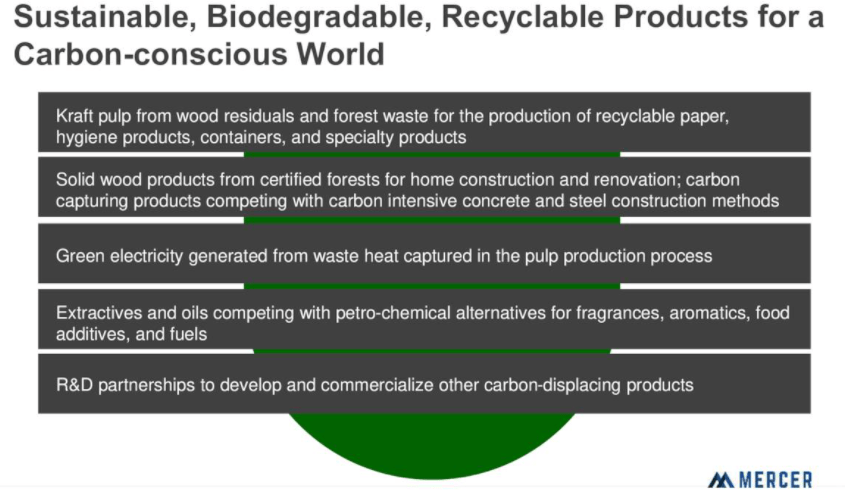

Innovative new forest products. (Mercer)

Innovative new forest products. (Mercer)

This article will start by directing our attention to those who are the direct stewards of our forests, Timber REITs. This article will not include operators with non-REIT status such as West Fraser Timber (WFG), Louisiana-Pacific (LPX), or Suzano (SUZ). Instead, I will be covering the landowners of Weyerhaeuser (WY), Rayonier (RYN), and PotlatchDeltic, who have obtained REIT status due to their ownership of millions of acres of land. In another article, I will discuss the other land operators and then look at paper product producers, mills, and distribution companies such as Mercer (MERC), UFP Industries (UFPI), and Boise Cascade (BCC), who may or may not also own and operate tracts of forest as well. Sorry to investors of CatchMark Timber Trust (CTT), recent poor performance has led me to not recommend the company.

Forests of North America account for 470 million hectares or 12% of the world’s forest resources (FAO, 2001). The extent to which these forests contribute to the economic, ecological, and social well-being of the United States and Canada depends, in large measure, on the policies and practices governing their management. States and provinces in North America have devoted significant effort over the last 20 years to define ecologically sustainable and socially acceptable timber harvesting and forest management practices.

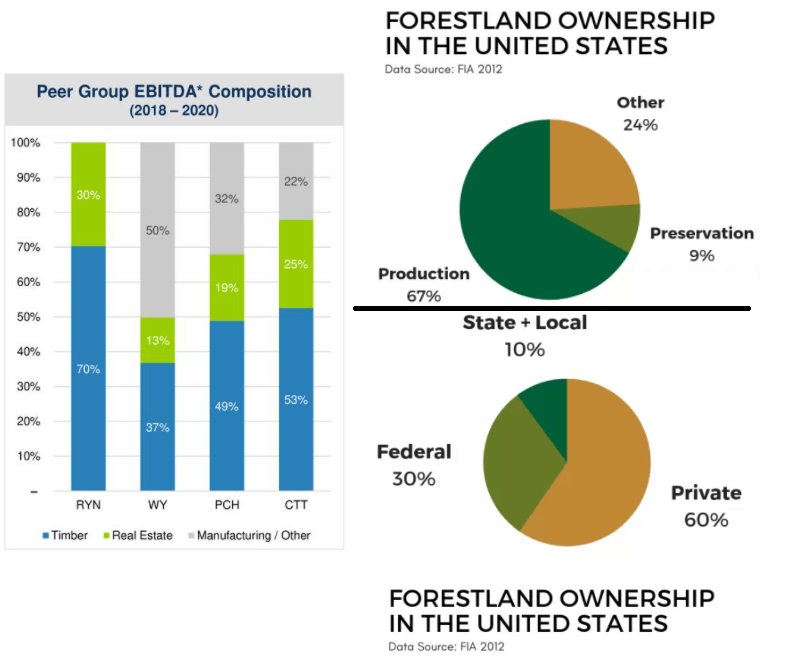

A Look at Timberland Ownership in the US (Image Compiled by Author. Data: Rayonier and National Association of State Forests.)

A Look at Timberland Ownership in the US (Image Compiled by Author. Data: Rayonier and National Association of State Forests.)

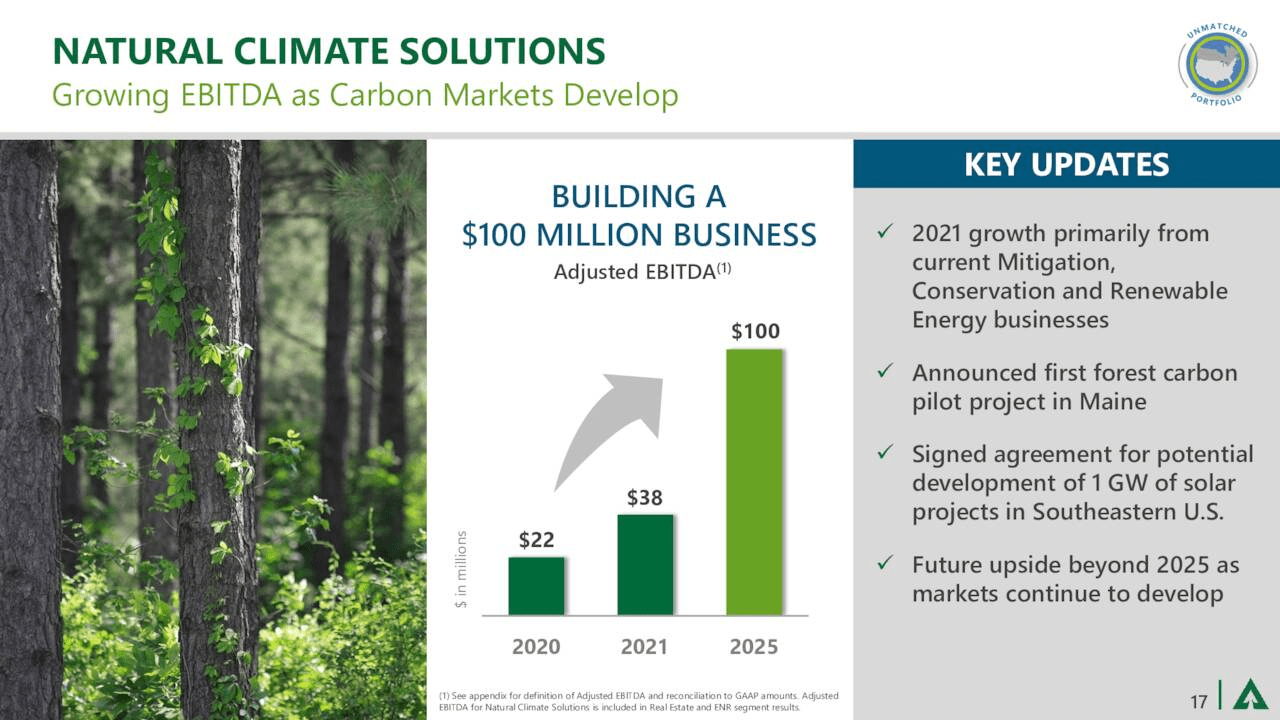

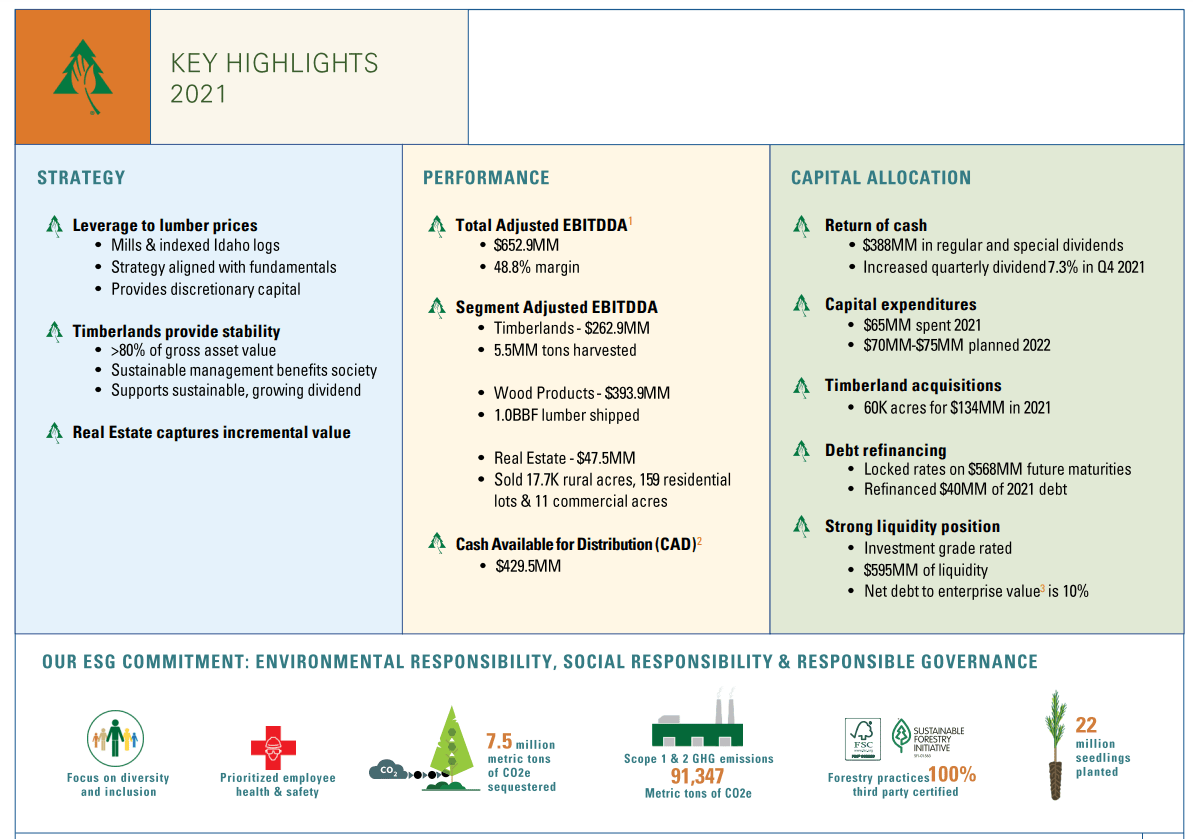

Information provided by the National Association of State Forests is quite useful for realizing that most logging is done by small-scale private practice. With approximately 50% of private forests being lots of less than 10 hectares in size, one can understand why most companies purchase logs on the open market. Major forest operators and owners are few and far between, and even they do not put 100% of their assets into timber production. Considering the three major timber REITs only own a combined 15.4 million acres out of over 400 million, they offer only a tiny overall exposure. This is due to the limited growth and economic viability that timberlands offer compared to other forms of real estate development, and I will discuss these opportunities with each company. Rayonier offers the highest exposure to the timber market, and so I will cover them first.

This company has ownership of 2.7 million acres world-wide (Pacific Northwest, US Southeast, and New Zealand) and approximately 70% of their EBITDA based on timber sales. While this exposure is far higher than peers, they do admit that non-timber real estate development from their land offers better growth of capital. This may be a risk to consider if you want to invest in a sustainable forest rather than another land development company. However, at the moment Rayonier is a leader in sustainable forest management, R&D, and efficient production for a public company, and worth an investment if this topic piques your interest.

Rayonier

Rayonier

While there are plenty of ethical merits, I will provide a quick summary of the financial state of the company. As a REIT, the major details are out of my purview, but there are plenty of other articles on SA for you to peruse. Due to changing timber prices, the 10-year growth rate of Rayonier is negative. However, over the past few years, there has been a positive growth cycle and three-year EPS and revenue growth has been over 10%. Part of the decline in growth is due to the sale of their mills and production sites, and the spin-off of Rayonier Advanced Materials (RYAM).

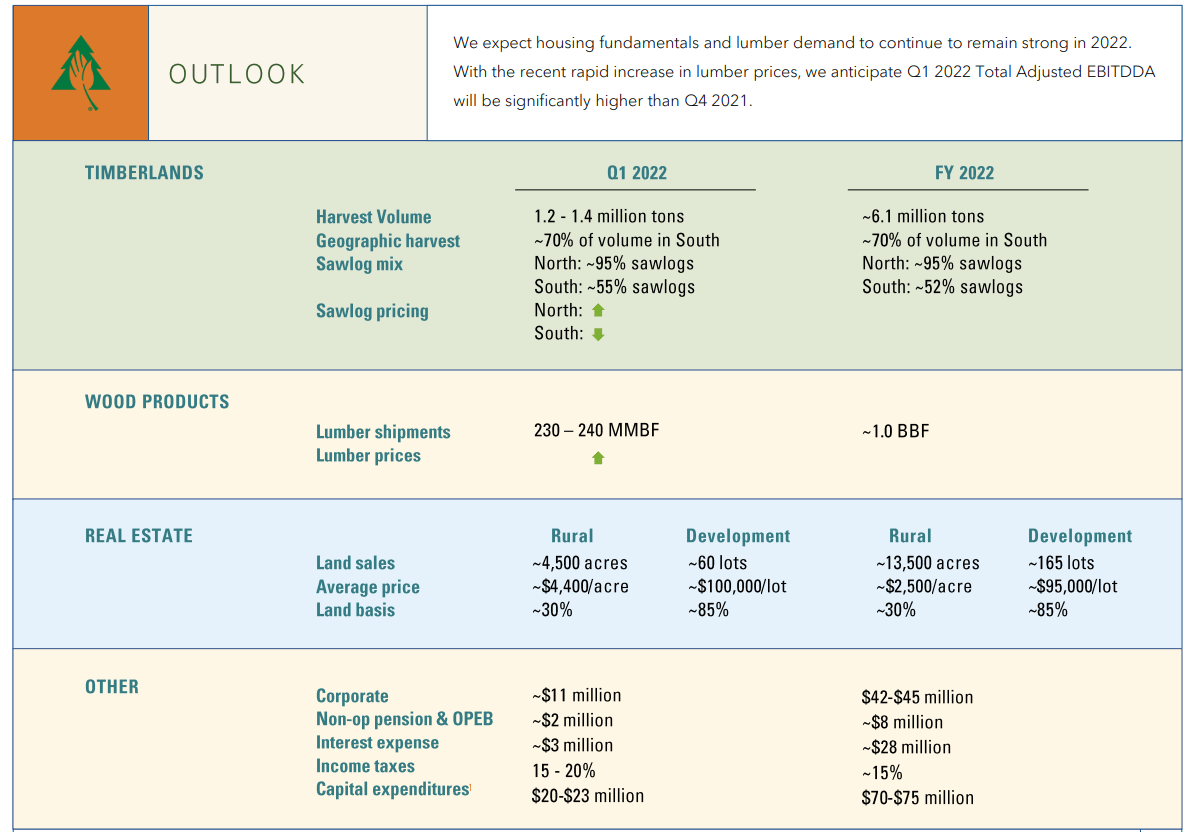

As a note towards volatility, growth is expected to decline YoY for 2022 by close to 50%. Outlook for growth is cloudy due to higher production and shipping costs, inflation, and poor demand in the US and China as growth slows after the pandemic boost. While worrisome, the company is rated well in the safety category with little debt and has no issues in providing consistent net income. Since the stock is at close to all-time-highs, I would hesitate to invest at the moment and wait for a positive outlook to resume in the future. Since forest product prices have remained elevated of late, it is possible for a change to their outlook at the next earnings, but it is best not to speculate. Those who set-up recurring investments after the price settles over the next few months may end up performing well.

One of the more famous names in the forestry REIT industry is Weyerhaeuser. The company has a long history of high performance and is loved by investors. However, the company is more diversified than Rayonier, which may be a consideration for some. I like WY since they are significantly carbon negative, own over 11 million acres of land in the US and operate in over 14 million acres in Canada, and are diversified into other positive land uses of renewable energy generation and conservation. Beyond owning and operating timberland, the company is also within the top 5 producers of lumber, OSB, and engineered wood in North America with their 19 mills.

With a best-in-class financial foundation, significant land ownership in NA, and ample diversification across wood product production, WY is great as the only forestry company in your company. While volatility has been an issue over the years, mostly thanks to the housing bubble in the 2000s, I believe EY offers a great long-term outlook and may end up less volatile than its peers.

Weyerhaeuser

Weyerhaeuser

Weyerhaeuser

Weyerhaeuser

The last forest owner I will cover is PotlatchDeltic, who own 1.7 million acres across the Northern and Southern US. The company owns far less acreage than WY, but also owns more processing mills than Rayonier. Therefore, the company is a hybrid between the two larger players. However, Potlatch has the lowest valuation of all the peers, especially compared to Rayonier. Considering the growth rate across the board for PCH is better over the past 10 years than the two peers, I believe the company offers the best risk/reward profile at the current share price. However, the major risk is the high exposure to Southern US timberland, and it will be important to watch the weather events in the region as they may have an undue effect on PCH.

PotlatchDeltic

PotlatchDeltic

PotlatchDeltic

PotlatchDeltic

The Timber REIT industry offers a unique environmentalism investment outside of the realm of EVs, renewables, and those ilk investments that are over-hyped in the current market. However, forestry has its fair share of risks to consider and work around, just like other commodities. Therefore, devout environmentalists and sustainable investment seekers will be the only ones who go along with these companies. Others should attempt to trade around the cyclicality of the market but I have few insights on commodity trading to share. However, I hope this article spurs you to continue down the research path if you find the sector of interest. Not to mention your investments will go a long way in developing sustainable forests while leveraging the rise in innovative new wood products. Perhaps the current upward cycle has a way to go.

While I have yet to choose my favorite holding in the industry, I will provide an update later on if I add any to my portfolios. The next article in this series will cover some other major land operators who also apply sustainable forest management techniques, but who operate the majority of their work on public lands in contract with government entities. Then, I will dive into the paper product developers and distributors to make sure they are doing their part to source sustainable wood products.

Stay tuned and thanks for reading.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of WFG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.