kotangens/iStock via Getty Images

kotangens/iStock via Getty Images

Resolute Forest Products Inc. (NYSE:RFP) gained over 133% during 2021 but remained down over 22% YTD. The plunge is due to the missed financial performance targets coupled with management guidance of headwinds relating to rising costs and uncertain logistics issues in 2022.

Despite the headwinds, the company’s core fundamentals remain strong, and the long-term trajectory remains positive. However, investors undesiring of high volatility stocks should be wary of the expected turbulence in stock prices throughout the year. As a result, I rate the stock with a strong buy rating, and I plan to place a limit buy order in the next 24 hours.

RFP reported revenue of $3.6 billion and a net income of $307 million, up 30% from $2.8 billion and over 30-folds from $10 million in FY2020, respectively. Despite this impressive growth in annual numbers and over 8% increase in Q4 revenue, the $128 million loss recorded during the quarter took a heavy toll on the company’s stock performance. The specifics of this loss have been discussed in the following segment, as it is tied explicitly to a non-recurring item.

The pandemic and the flooding in BC, CA caused major operational difficulties to the company as the logistics and labor issues raised the manufacturing and freight costs, bearing down on the company’s operating income. However, as the pandemic subsides and logistic routes start rebounding for the upcoming construction season, we should start to see the effects negated from the company’s financial performance, substantially raising the operating income.

The company’s revenue increase is primarily attributable to increased prices and surging demand for wood products, especially in the home building industry. These factors have shielded the company against the operational hurdles through the fourth quarter and are a relevant source of sustainable revenue growth in the coming quarters.

The fourth-quarter loss was significantly attributable to the closure of the company’s Pulp and Paper operations at their Calhoun, TN mill, which led to a one-off closure charge of $142 million and inventory write-offs of $29 million. Excluding these items, the company would’ve reported a net income of $43 million, a significant improvement from the $52 million net loss in Q4 2020. This $171 million charge amounts to over 80% of the non-recurring charges recorded throughout the year. The adjustment turns the annual net income of $307 million into $480 million with a net margin increase of 4.7% from 13.1% against a current margin of almost 8.4%.

This closure is also expected to reverberate in the current quarter as the company continues to post decommissioning charges. However, this closure is expected to significantly improve the company’s future profitability. The plant was responsible for over $60 million in operating loss by the end of Q3 2021 on a TTM basis. The company has suggested that this move is likely to result in a $35 to $40 million improvement in the company’s overall operating income. As a result, this reflects the ‘lost pulp integration benefit with its tissue manufacturing of approximately $15 million and approximately $5 million from ongoing costs associated with closed site maintenance.’

This improvement in operating income suggests an over 35% increase in the company’s annual operating income. Suppose these figures show up during the current year’s financial statements. In that case, it will hedge positively against the headwinds identified by the company in 2022, directly shielding the company from the stock price blowback seen after the Q4 results announcement.

The company’s financial position continued to grow stronger throughout the year with greatly improved leverage, liquidity, and efficiency ratios. The company has continued to mitigate its liabilities throughout the year. It has toned down its total debt to $302 million, down 46% from Q4 2020, leading to a low debt-to-equity ratio of under 20%. This improving leverage has also resulted in a consistently decreasing interest expense which has come down almost 40% YoY from $34 million 2020 to $21 million in 2021.

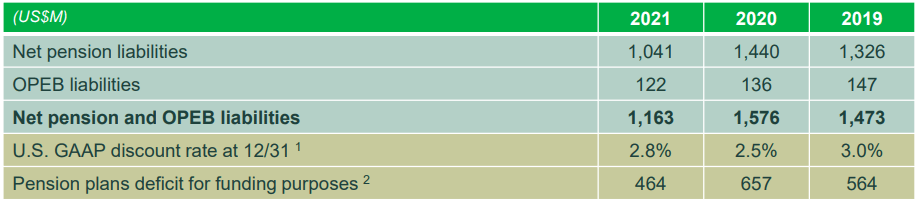

RFP’s pension fund liabilities have steadily declined as part of the low debt ratio. They have reduced from $1.5 billion in 2020 to $1.1 billion in 2021, a YoY decrease of over 26%, with the underfunding gap reduced to $464 million (down over 29% in 2020, from $657 million).

Net pension liabilities

Net pension liabilities

Source

A low debt ratio opens the company up to either add more debt financing into the mix and return more excess capital to the shareholders, effectively decreasing the cost of capital and improving financial performance metrics, including EPS, etc., or keep the debt ratio down to safeguard itself against the economic downturns, which currently makes a lot of sense because of the global volatile economic conditions.

RFP has also continued to significantly improve its liquidity, despite the cash and cash equivalent decreasing from $113 to $112 at year-end. Even a $112 million balance means that almost 13% of the company’s market cap is available in cash. In addition, with access to revolving credit facilities of about $841 million, RFP’s liquidity is close to a billion dollars, carrying a current ratio of 2.29 and interest cover of over 14.

One of the major ways the company can utilize this cash is by looking into further transactions inside the Unites States, like the Conifer Timber Inc. acquisition, to overcome the duties issues as the company is currently paying the highest duties of any Canadian company at almost 30%. So even though it’s a political issue and the company is working on a resolution, it would be a practical step to increase their production and overall foothold inside the United States, a much bigger market than Canada.

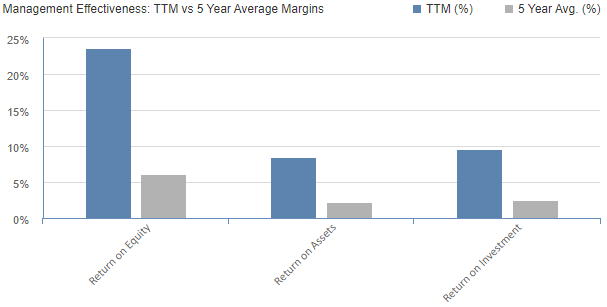

The company’s ROE, ROA, and ROI also stand at higher levels than its 5-year average at 23.66%, 8.5%, and 9.58%, respectively, signifying a massive improvement in resource utilization of the company’s capital. The company hasn’t seen such metrics since 2011.

Management Effectiveness

Management Effectiveness

Source

Because of the 20% decline in the company’s share price since their financial results on February 3rd, RFP has become even more attractive in its valuation measures since I last reported on the company. With a P/E ratio of less than 3, a P/S ratio of 0.24, and a P/B ratio of 0.60, the market hasn’t priced in the upside potential held inside the stock.

This valuation is reflected in the aggressive increase of RFP stocks in hedge fund portfolios with BNP Paribas Arbitrage, Royal Bank of Canada, Morgan Stanley, Wells Fargo, and Bank of America, all raising their stakes in the company. As a result, the company has an overall “outperform” or “buy” analyst rating.

My previous analysis reflected macroeconomic conditions such as the housing boom and increasing pulp and lumber prices. In contrast, this article purely focuses on its solid fundamental strength and its ability to sustain its positive performance for the foreseeable future. The company’s leverage, liquidity, efficiency, and profit margins are the highest in over a decade. This continuing growth and improvement are likely to be sustainable and consistent through strategic maneuvers which are already apparent, such as the closure of the Calhoun plant operations.

I have already covered the share buyback scheme, which resulted in the company acquiring 4.6 million shares (6%) in 2021 and further planning to buy back 10 million shares or $100 million worth of stock. With the increasingly strong market demand coupled with operational efficiencies, underlying fundamental strength, and low valuation metrics, the share price is bound to catch up and price in the upside potential, which will likely result in significant investor gains.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in RFP over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I plan to place a limit buy order in the next 24 hours.