Central European roundwood markets are at a turning point as forests in much of the region have recently suffered extensive damage from a bark beetle outbreak, leading to temporary increases in harvest, lumber production and log export. Central European wood supply is expected to decline towards 2030 in the wake of the outbreak.

And new forest management practices to minimize the risk of future outbreaks will have long-term implications for wood quality and availability.

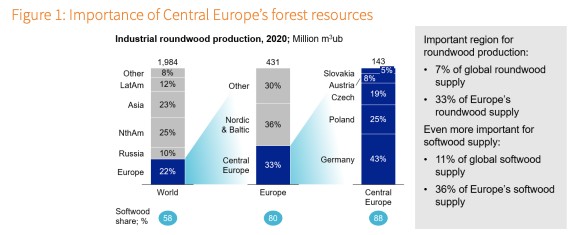

An important softwood basket

Central Europe is home to an important forest resource for industry in the region, and the supply of wood product globally. Germany, Austria, Poland, Czech Republic, and Slovakia represent 33% of European roundwood harvest.

The region is especially important for the supply of softwood logs and lumber; almost 90% of harvest is softwood species, such as pine and spruce, and the region represents 11% of global softwood supply (Figure 1). More than half of harvest is sawlogs, supplied to sawmills producing about 14% of global softwood lumber supply.

But the region faces several unique challenges. Sawlog and pulplog prices are among the highest in the world, due to a combination of tight markets with a well-developed forest products industry, a large share of public forests not managed intensively for production, and a highly fragmented private forest ownership base. In Germany, Czech Republic and Poland, the average size of a private forest holding is less than 3 hectares. The small scale creates challenges for cost-efficient forest management, harvesting and log transport. Many forest owners are absentee, living far from their forests.

The spruce bark beetle outbreak

Since 2018, the greatest challenge to forest management in Central Europe, is the spruce bark beetle. This is a species (Ips typographus) endemic to Europe, but one with a population explosion in 2018 following an unusually dry and warm summer. In the four years 2018 to 2021, an estimated 360 million m3 of timber has been damaged by bark beetles – equivalent to about 2.3 years’ harvest. While there are other bark beetles damaging European forests, including species adapted to pine and larch trees, more than 85% of damage in Central Europe in 2018-20 was caused by the spruce bark beetle.

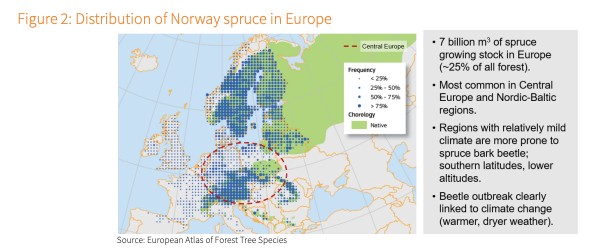

Central Europe is particularly prone to the bark beetle outbreaks, for two reasons. Firstly, Norway spruce is a very common tree species in the region (Figure 2). It represents about 60% of forest stock in Austria, 54% in Czech Republic, and 26% in Germany. Spruce is native to the region and has become even more common due to its commercial value. The second reason is that spruce bark beetles thrive in relatively mild climates; while spruce is also common in the Nordics, Baltics and Russia, spruce bark beetle damage there (so far) has been far more limited. Forests at higher altitudes in Switzerland and Austria are also less affected.

Initial impact on wood markets

One result of the bark beetle outbreak has been an increase in harvests and wood supply (Figure 3). Damaged forests need to be harvested both to prevent spread of the beetle and to salvage sick and dead trees before began to decay. Annual harvests increased by 20-30 million m3 during 2018-21. At their peak in 2020, harvests were almost 20% higher than pre-outbreak levels. Even though harvesting was focused on damaged stands (about 70% of harvest in Germany in 2020 was damaged timber), not all damaged trees were salvaged in time. This led to “two-tier” pricing of sawlogs, with lower prices for drier damaged logs.

With an increased supply of logs, prices declined in 2019 and 2020. Log exports also grew, both to neighbouring countries in Europe and internationally. Softwood sawlog export from Central Europe to China grew from very low levels pre-outbreak, to 8 million m3 in 2020. Fortunately, the latter years of the outbreak coincided with a global COVID-related rally in lumber markets. Sawlog demand in Central Europe was very strong in 2021 with expanded lumber production, leading to a log price recovery. Lumber exports also grew, primarily to China and the US.

Outlook for wood supply

Bark beetle damage in Central Europe peaked in 2019 (Figure 4), and we forecast damage to return to near normal levels by 2025. The most susceptible stands have already been infected, and forest owners have become better at managing the outbreak. Harvesting will therefore decline, with less need for sanitary and salvage removals. Indeed, harvests have already fallen from their peak levels, by 3% in 2021 and an expected 4% in 2022 (versus 2020). Reverting to pre-outbreak harvest levels would imply 16% lower wood supply.

There is also a real risk of long-term lower harvest potential in Central Europe. In the study, we present several scenarios for future wood supply development, considering the reduced availability of harvest-age forests, forest utilization rates, EU forest policy, public and private forest owner responses. In one scenario, supply will fall to well below pre-outbreak levels by 2030. Interviews with industry participants also reveal concern about future log supply, especially to the recently expanded sawmill industry.

Longer-term, adapted forest management to reduce the risk of future bark beetle outbreaks will also impact wood markets (Figure 5). These include a more diverse species mix with reduced share of spruce, shorter rotations with smaller log diameters and higher yield, and more active management of even small private forests holdings.

Global implications

Reduced harvest in Central Europe in 2025-2030 will impact softwood log and lumber markets globally. Log exports from the region grew from 11 million m3 in 2015 to 33 million m3 in 2021, mainly from Germany and the Czech Republic. Net export is expected to swing back to net import, causing tighter softwood markets in Europe and beyond. China has been a significant recipient of Central European sawlogs and will be challenged to replace these volumes with imports from other key sources, including New Zealand, Russia and the USA. Competition on European markets will likely intensify as Chinese imports seek to outprice domestic buyers.

Sawmills in Central Europe will face both higher sawlog prices and lower sawlog availability, threatening their cost position, and in some cases, their continued operation. Lumber exports from the region, which grew by 4 million m3 in 2016-2021, probably cannot be sustained at current levels – especially now when the war in Ukraine will lead to reduced lumber imports to Europe from Russia, Belarus, and Ukraine. This will in turn impact lumber markets in the US and China, which have grown to depend on lumber imports from Europe.

The post Central European roundwood markets are at a turning point appeared first on Global Wood Markets Info.