Inflationary pressures from the central bank and government liquidity and stimulus have lit a bullish fuse under the commodities asset class. Gold was the first commodity to take off on the upside, rising to a new record high in August 2020 in all currency terms. In 2021, many other commodities followed in what became a bullish relay race where one raw material market seemed to hand off the bullish baton to another. Grain and oilseed prices rose to over eight-year highs. In May 2021, lumber, copper, and palladium prices reached all-time highs. As they corrected, other commodities moved to the upside. In July, August, and September, crude oil, natural gas, coffee, sugar, and FCOJ moved to the highest prices in years.

Lumber was in the market’s spotlight when the price exploded to its highest level ever at over $1,700 per 1,000 board feet in May. An almost perfect bullish cocktail of rising inflationary pressures, COVID-19 inspired supply bottlenecks, increasing demand for new housing as interest rates were at the lowest level ever, and the potential for a US infrastructure rebuilding initiative lifted wood’s price to a peak in a parabolic move. Gravity hit the lumber market after the May high, and the shooting star became a falling knife.

The iShares S&P Global Timber & Forestry Index ETF product (NASDAQ:WOOD) holds shares in leading lumber companies whose fortunes tend to rise and fall with the price of wood. WOOD tends to track the price of lumber futures with far less volatility.

I have traded almost every commodity on the world’s futures exchanges over the past four decades. Meanwhile, I have never bought or sold one contract of lumber. Lumber’s liquidity makes the futures contract a benchmark instead of a trading vehicle.

Illiquid markets are worse than roach motels. It is easy to get into a roach motel, but leaving alive is doubtful. In lumber, it can be impossible to execute a buy order when the market is rising or a sell order when it is falling. Getting out of the wrong risk position can be more than a challenge as lumber tends to gap higher or lower to exact the most pain from trapped in adverse long or short positions.

Lumber is a feast and famine futures market. During selloffs, the price can drop to irrational, illogical, and unreasonable levels and rise to insane prices during rallies. In late February 2020, lumber traded to a high of $468.30 per 1,000 board feet. A little over one month later, the wood futures fell to $251.50 during the height of risk-off selling at the beginning of the global pandemic.

The March 2020 low gave way to the most significant rally in the commodities asset class in recent memory. Lumber, an obscure industrial futures market, moved into the spotlight on financial news networks. It also became the poster child for the US central bank.

Source: CQG

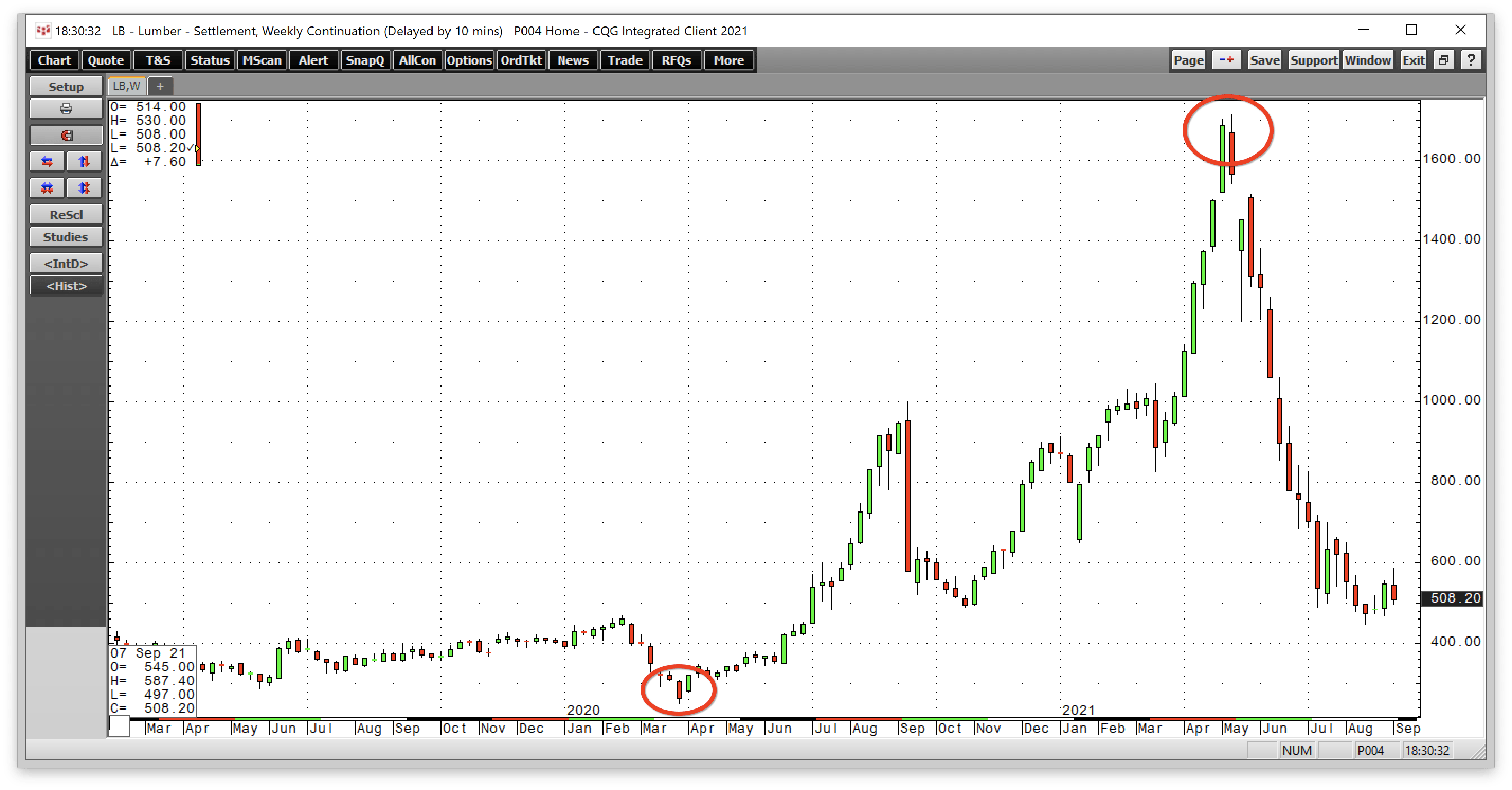

As the weekly chart illustrates, lumber moved over 6.8 times higher from the March 2020 low to the May 2021 high, with the bulk of the move starting in late October 2021 at below $500 per 1,000 board feet. Few markets, aside from the wild cryptocurrencies, have experienced price appreciation like lumber. Like most shooting stars, lumber collapsed after reaching the $1711.20 high in May 2021. By mid-August, the price dropped to a low of $462, less than one-third the price at the high.

Source: CQG

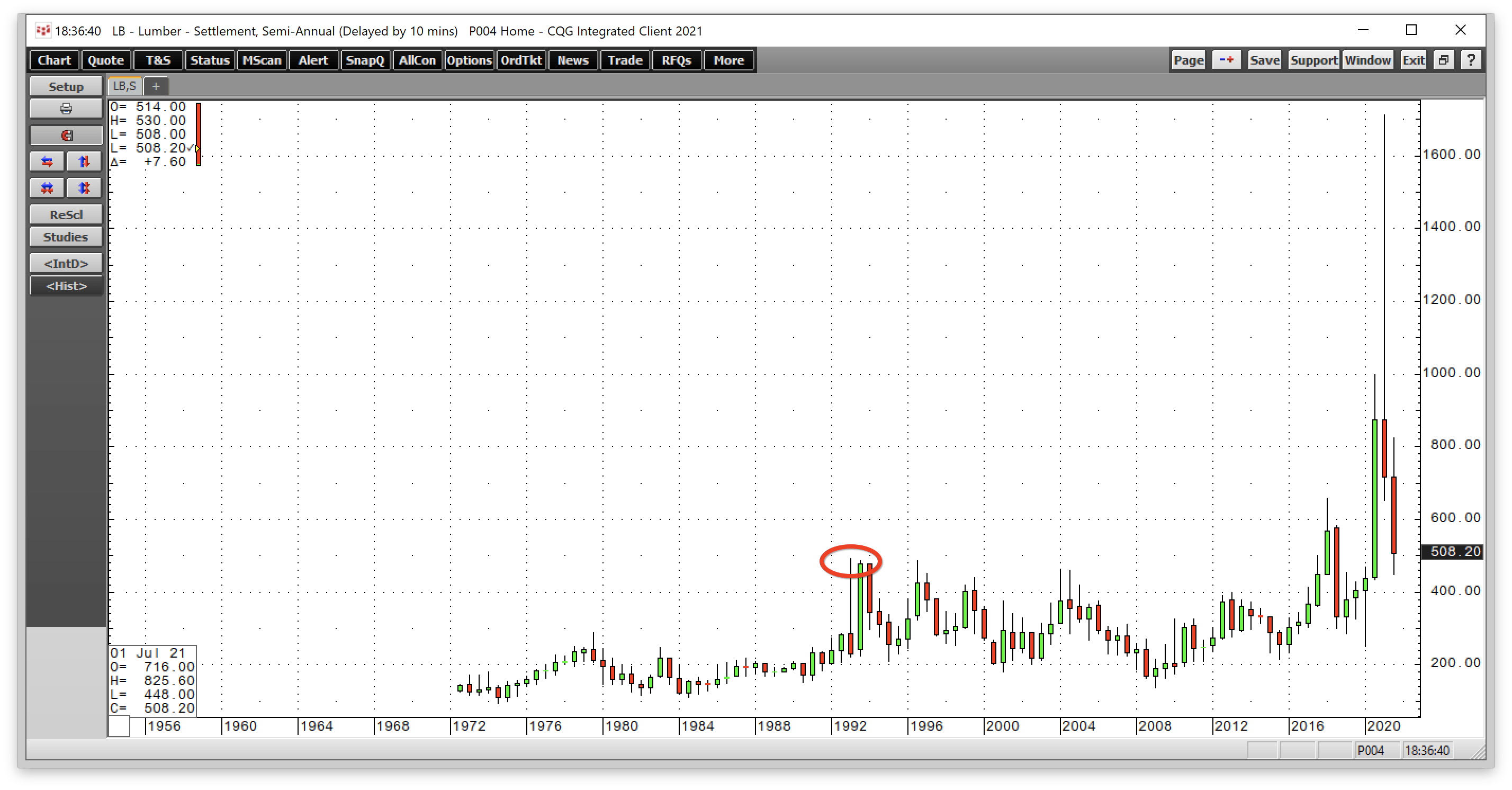

The semi-annual chart shows that before 2017, the all-time peak in the lumber futures arena was at the 1993 $493.50 high. At over $500 on the nearby futures contract at the end of last week, lumber may still be under one-third the price at the May peak, but it is still over the record level before 2017.

The daily chart of lumber futures shows that the $1711.20 high caused a severe backwardation where nearby prices traded at a considerable premium to deferred prices in May.

Source: CQG

The chart of the active month November futures shows the May high only reached $1400 per 1,000 board feet, a $311.20 discount to the continuous contract. The backwardation signified that market participants believed the supply shortage would diminish, as higher prices lead to more output. The November contract still dropped to one-third the level at the high when it reached a low of $462 on August 20.

I may never trade lumber, but I watch the price action like a hawk. Markets that magnify sentiment can be incredible barometers that signal price trends in other related assets.

I view the $462 August 20 low as a significant level in the lumber market. The price briefly dropped below the pre-2017 record high and turned high. On September 10, lumber futures closed at the $607.60 level after trading to a high of $695 per 1,000 board feet on September 7.

The bullish relay race in commodities began with the March through May 2020 pandemic-inspired lows. The first commodity futures market that rose to a new record high was gold. The precious yellow metal reached $2063 per ounce in August 2020 before correcting. While gold fell, it handed the bullish baton to other asset class members.

In 2021, grain and oilseed futures prices rose to an over eight-year high before correcting. In May 2021, lumber, copper, and palladium made record highs. NYMEX crude oil futures made a marginal new high in early July, rising to its highest price since 2014. In July and August, coffee, sugar, and frozen concentrated orange juice futures moved to the highest prices in years. The latest baton holder has been natural gas, rising to its highest price at over $5 per MMBtu last week, the highest price since February 2014. Meanwhile, coal is trading at a thirteen-year high, iron ore, steel, and most nonferrous metals are at levels not seen in many years.

The tidal wave of central bank liquidity and tsunami of government stimulus are inflationary seeds. Even if the Fed begins tapering its quantitative easing program where it is purchasing $120 billion in debt securities each month, tapering is not tightening. Moreover, an infrastructure rebuilding program and a multi-trillion-dollar federal budget are fiscal stimuli that will continue to fertilize inflationary pressures.

Ironically, the Fed cited the lumber market as why the central bank believes inflationary pressures are “transitory.” Fed Chairman Jerome Powell pointed to bottlenecks at lumber mills as the reason for the rise. As lumber’s price declined, it gave the central bank a false sense of security. However, the Fed never mentioned that lumber is a highly illiquid market and a roach motel.

The daily chart shows that the total number of open long and short positions in the lumber futures arena stood at 1,869 contracts at the end of last week. Crude oil’s open interest was over 2.15 million contracts, gold futures were at over 299,000, and copper’s stood at over 196,000 as of September 10. Even the less than liquid frozen concentrated orange juice market had over 11,500 contracts long and short open contracts. Moreover, on Friday, September 10, 272 lumber contracts traded in the futures market. A day when over 1,000 lumber contracts change hands is the exception, not the norm. On a typical trading day in the NYMEX crude oil arena, over one million contracts trade.

Inflationary pressures continue as one commodity passes the bullish baton to another. We are moving towards a time of year when construction demand tends to decline during the winter months. However, once spring is on the horizon, expect lumber to retake the bullish baton. Interest rates remain at historically low levels, and real estate demand is booming. New home construction and a US infrastructure rebuilding initiative will require lots of lumber, which could light another bullish fuse under the illiquid market.

If lumber offered the potential to execute buy and sell orders, I would be a buyer below the $500 level. While I do not trade lumber, I take risk positions in more liquid proxies that correlate with wood prices.

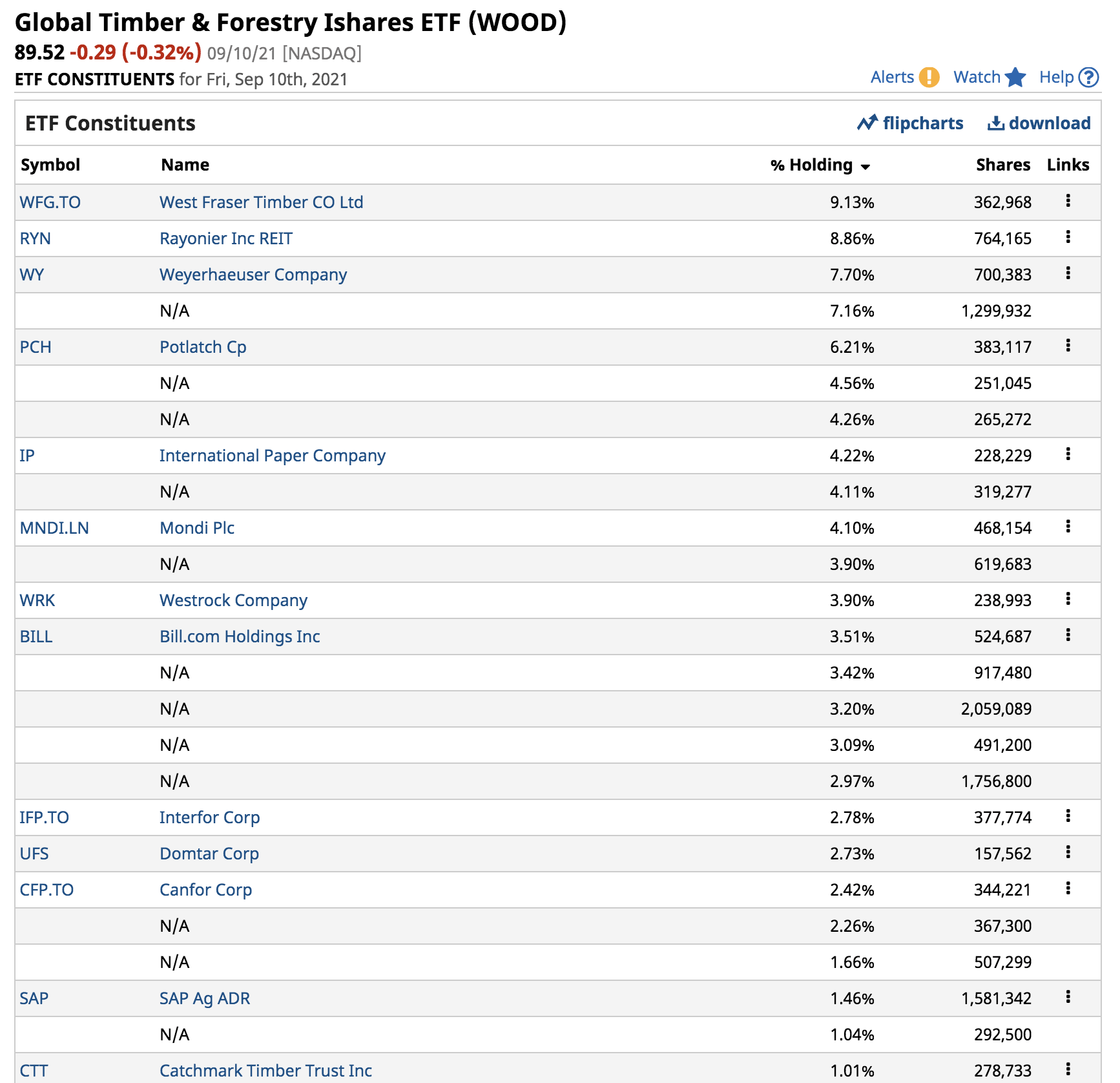

The top holdings of the iShares S&P Global Timber & Forestry Index ETF product include:

Source: Barchart

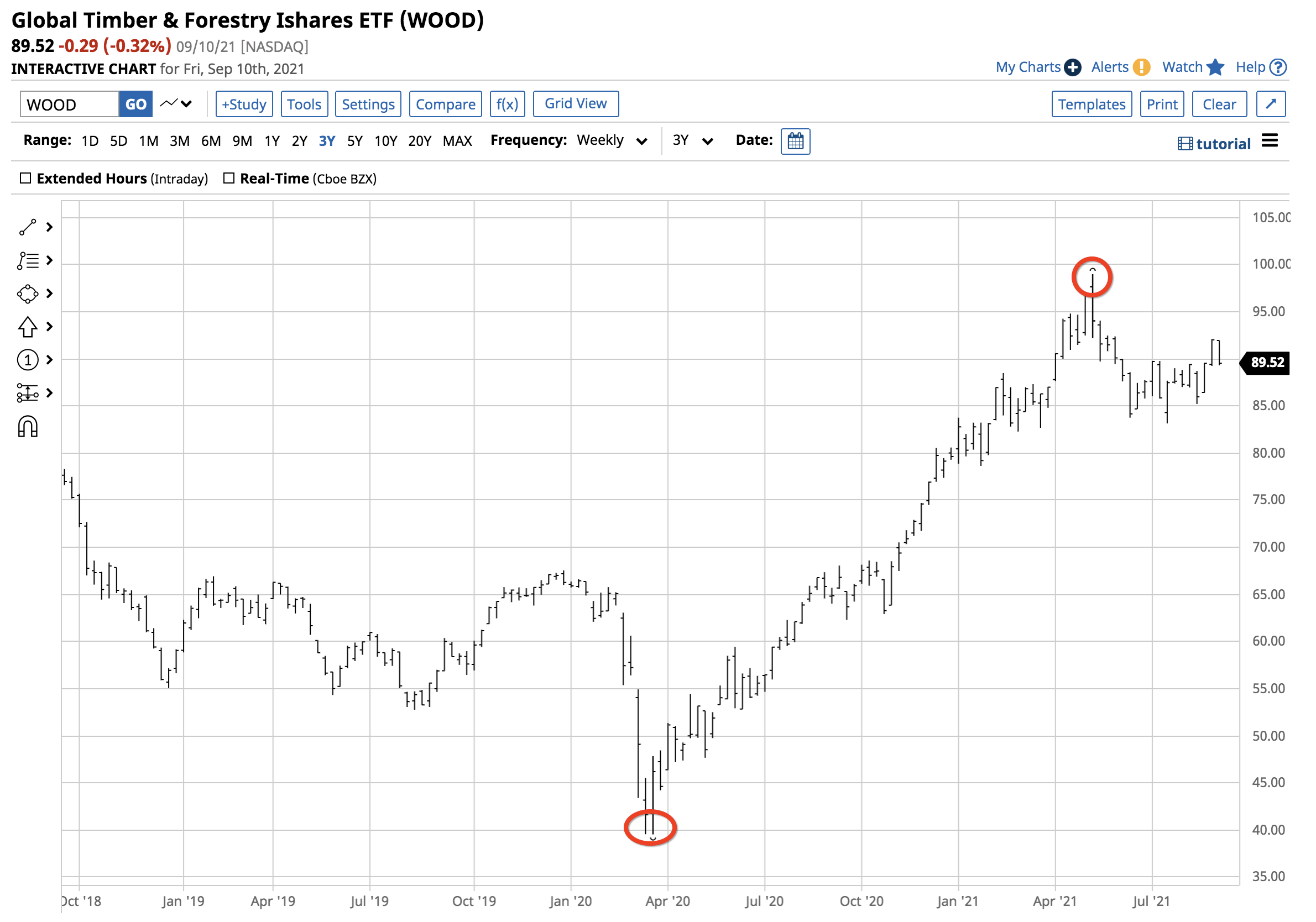

The WOOD product had $317.396 million in assets under management at $89.52 per share on September 10. WOOD trades an average of 25,465 shares each day and charges a 0.46% management fee. The blended yield of $1.17 per share or 1.31% offsets the management fee over time.

Source: Barchart

As the chart shows, WOOD exploded higher from a low of $39.55 in March 2020 to a high of $98.98 when lumber reached its high in May 2021. The 150.3% gain underperformed the illiquid lumber market on the upside. However, at $89.52, WOOD was 9.6% below the May high, far outperforming the lumber futures arena on the downside. WOOD invests its assets in lumber-related REITS and companies with direct exposure to the wood market.

I expect the lumber price to rally and reach at least the $1000 level during the first half of 2022. Inflationary pressures, low interest rates, the demand for new housing, and US infrastructure rebuilding create a potent bullish cocktail. Lumber prices could retest the recent lows as it waits to receive the bullish baton, but any price weakness is likely to be a buying opportunity. I will never buy or sell one contract of lumber futures, but WOOD is an excellent proxy that correlates well.

The Hecht Commodity Report is one of the most comprehensive commodities reports available today from a top-ranked author in commodities, forex, and precious metals. My weekly report covers the market movements of over 20 different commodities and provides bullish, bearish, and neutral calls; directional trading recommendations, and actionable ideas for traders.

This article was written by

Andy spent nearly 35 years on Wall Street, including two decades on the trading desk of Phillip Brothers, which became Salomon Brothers and ultimately part of Citigroup.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The author always has positions in commodities markets in futures, options, ETF/ETN products, and commodity equities. These long and short positions tend to change on an intraday basis.