The European parquet market progressed significantly in 2021 and reached level not seen since 10 years While an increase in parquet consumption was expected in 2021, reflecting a compensation of the impacts of Covid-19 and the related measures, such as lockdowns, taken in 2020 in some Federation of European Parquet (FEP) countries, we observe that consumption is higher than in 2019, before the pandemic, and even reaches a level not seen since 10 years.

After a stable-to-positive year in 2020 (+1.3%), the European consumption of parquet rose by 6.2% in 2021. Consumption of parquet has increased on almost all European markets especially during the first semester, when compared to the same period in 2020. During the rest of the year, demand continued to grow but at a slower pace as consumers restarted to dedicate their spendings to areas such as leisure and travels. Nevertheless, renovation, and adaptation of homes to “post-Covid-19” life, remains the driver of the parquet consumption growth.

As usual, the results show variations from country to country. Countries such as Italy and France, which were not able to offset the loss experienced during the spring 2020 lockdown and reported declines in parquet consumption for the year 2020 as a whole, are showing large increases in parquet consumption in 2021 compared to 2020. Croatia, Romania and Switzerland are also reporting significant increases in parquet consumption while Portugal is focusing more on exports.

On the other hand, countries which totally, or partially, compensated, during the second half of 2020, the bad performance observed in March-April of the same year, generally report lower but still sustained rising rates. This is the case of Scandinavia, Austria and Spain, while the German parquet market stabilizes.

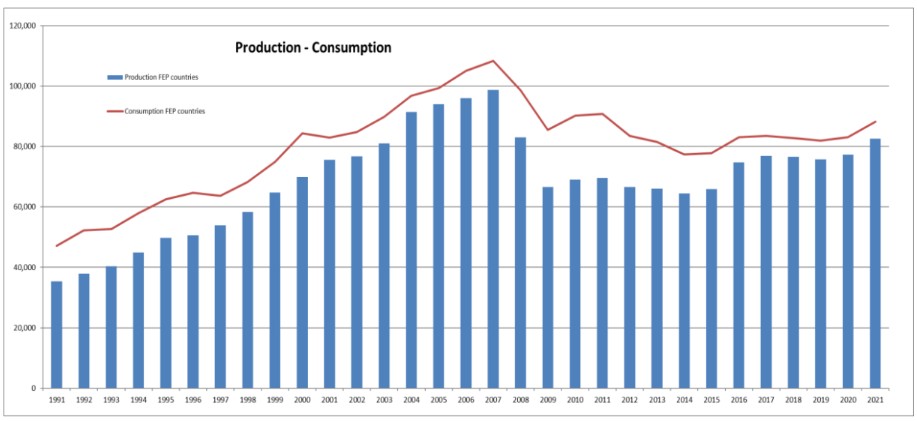

The production in FEP territory rose by almost 7% in 2021 and exceeded the 82 million square meter threshold. A level not seen since the start of the financial crisis. The European production outside FEP countries is at an estimated 15.3 million square meters – 9.7 million square meters produced in EU countries and 5.6 million square meters in European non-EU countries.

The total production in FEP territory significantly increased (+6.92%) in 2021 to a volume of 82,624,000 m2. Taking into account the total production in Europe (FEP countries + non-FEP countries in Europe) implies that production in 2021 rose by 7.88% and reached almost 98 million m2.

The 2021 total parquet production per type remains similar to the picture already presented from 2010 onwards, whereby multilayer comes in first with 83% (compared to 82% in 2020), being followed by solid (including lamparquet) at 15% (compared to 16% in 2020) and mosaic with a stable 2% of the total cake.

In absolute production figures by country, Poland maintains its top position at 16.06%. Sweden keeps its second place on the podium with 14.94%. It is followed by Austria at 13.00%, while Germany comes in as fourth (9.94%).

Consumption in FEP area also increased significantly in 2021 (+6.18%) and reached 88,155,000 m2 compared to 83,023,000 m2 the year before.

In terms of consumption per country, Germany keeps its first position with 20.45%. Italy at 10.49% and France at 10.19% overtake Sweden (9.88%). Austria with 7.73% remains in fifth position while Switzerland (7.45%), the Nordic Cluster (6.81%) and Spain (6.49%) follow.

As regards the per capita parquet consumption, Sweden keeps the first seat (0.86 m2 ) before Estonia (0.77 m2 ), Austria (0.76 m2) and Switzerland (0.75 m2 ). In the total FEP area, the consumption per inhabitant slightly increases at 0.21 m2 in 2020 and 2021.

The usage of wood species in 2021 as shown on the above graph indicates that the share of oak remains stable at 81.9% compared to 81.8% in 2020. Tropical wood species represent 2.1% of used wood. Ash and beech are still the two other most common chosen species with 5.3% and 2.8% respectively.

Outlook for 2022 & 2023

The European parquet markets show diverse evolutions for the first quarter 2022 compared to the same period last year. While Italy, Scandinavia and Spain report still significant increases in demand, Benelux, France and Switzerland present flat evolutions. On the other hand, Austria and Germany are already experiencing decreases, reflecting the difficulty to fill in orders. This phenomenon is expected to be reported by all markets in the coming months as most of the FEP members are facing issues of wood supplies.

Issues of wood & wood products availability and affordability are limiting the positive evolution of the parquet industry since the outburst of the pandemic, reflecting high demand for wood and supply chains’ disruptions, but they are now getting even more acute with the geopolitical turmoil. A significant part of wood raw material and semi-finished products used by European parquet producers came from Ukraine, Russia and Belarus. These trade flows have been impacted by the situation and the related measures.

Due to the already very tense situation on the wood markets and the ecological responsibility, it is not possible for the sector to fully diversify sources of wood to other species and/or other countries.

FEP is thus asking the EU authorities for temporary safeguarding, mitigation and support measures to the sector, for a tool, such as a quota, to keep oak logs within Europe and for coherent policies allowing higher mobilization of existing European wood resources (Forestry Strategy, Biodiversity Strategy…) as long as principles of Sustainable Forest Management are applied. A longer-term perspective to explore sustainable (and recyclable) substitutes and alternatives to oak should also be adopted.

The post Significant progress in the European parquet market; outlook uncertain appeared first on Global Wood Markets Info.